Introduction

The landscape of real estate financing is constantly evolving, influenced by numerous economic factors and central bank policies. Understanding current mortgage rates is crucial for potential homeowners and investors alike, especially in light of changing market dynamics. As of October 2023, fluctuations in mortgage rates are more relevant than ever, given the rising cost of living and prospective changes in the Federal Reserve’s monetary policy.

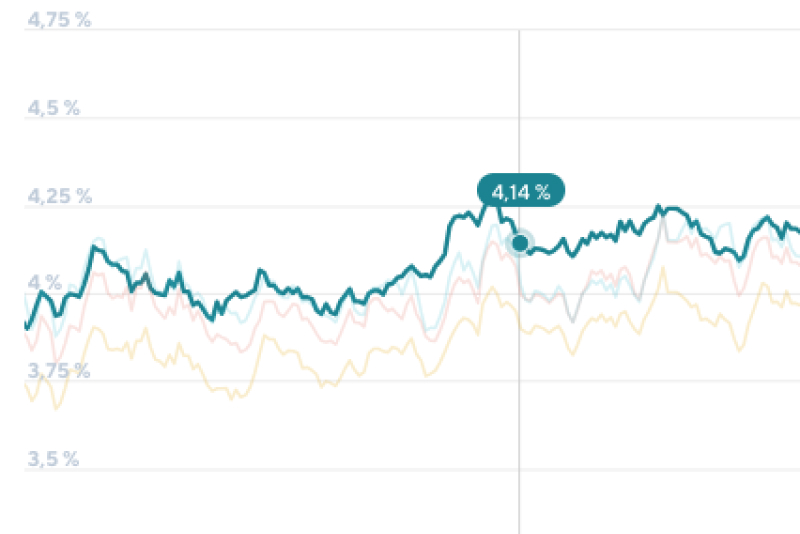

Current Trends in Mortgage Rates

As of mid-October 2023, average mortgage rates for a 30-year fixed-rate mortgage hover around 7.5%. This represents a considerable increase compared to rates observed in early January, where the typical rate was about 6.0%. Similarly, 15-year fixed mortgage rates are averaging around 6.7%, showing a similar upward trend. The increase in rates is largely attributed to inflationary pressures and the Federal Reserve’s ongoing interest rate hikes aimed at stabilizing the economy.

Factors Influencing Mortgage Rates

Several factors impact mortgage rates, including economic indicators, inflation, and the Federal Reserve’s interest rate policy. The recent CPI (Consumer Price Index) reports show persistent inflation, compelling the Fed to increase interest rates to bring prices under control. Furthermore, geopolitical uncertainty and changes in the global economy also play a significant role, as market sentiment can lead to fluctuations in lending rates. Analysts project that if inflation continues at its current pace, mortgage rates may rise further before stabilizing, making it essential for homebuyers to monitor these developments closely.

Impact on Homebuyers and the Real Estate Market

The surge in mortgage rates has profound implications for homebuyers. High rates mean increased monthly payments, which can further strain the budgets of families already dealing with rising costs of goods and services. Potential buyers are finding it increasingly difficult to secure affordable financing, resulting in a cooling housing market. According to recent data from the National Association of Realtors, home sales have declined by approximately 20% year-over-year, largely reflecting buyer reluctance due to elevated borrowing costs.

Conclusion

As the real estate market continues to adjust to the higher current mortgage rates, both buyers and sellers are being forced to reconsider their strategies. Experts suggest that potential homebuyers should remain vigilant, considering their options carefully and possibly locking in rates if they are able. Looking ahead, many speculate that if inflation shows signs of decline, we may witness a stabilization of rates in late 2023 or early 2024. Until then, navigating the housing market will require a careful approach and informed decision-making.